India Remains a Fantastic Long Term Compounding Story- Q&A with Mr. Nilesh Shetty

Posted On Monday, Aug 17, 2020

The current economic crisis is an opportunity amidst turmoil if you look through the lens of a value fund manager. Managing our flagship fund Quantum Long Term Equity Value Fund for almost a decade. Mr. Nilesh Shetty shares his insights. In this exclusive Q&A he tells us why a Value style of investing has an edge in times of distress. Read on to know more.

Q1. You are a value style Fund Manager. What does that really mean in practice? How do you, a value investor, see the current environment?

Value style fund managers are essentially trying to ensure they don't lose a lot of money in the process of investing. Our strategy remains to identify good companies and try and buy them at a discount to their fair value. If the investment thesis doesn't work out as planned, the fact that we have not overpaid for the investment gives us some downside protection. If the thesis woks out as we had foreseen, the market over time will ensure these companies trade close to their fair value allowing us to make decent returns without taking significant risks. Hence the process of stock selection becomes fairly predictable. In markets where risk aversion is very high and companies trade at large discounts to their fair value, you can expect us to be aggressive buyers and in euphoric markets, where no one believes stock prices can ever fall, the fund will be selling stocks which are overvalued and wait on the side-lines.

The Covid related correction has allowed us to buy great businesses at reasonable valuations. We expect most of the companies we own will not only survive but thrive in the post Covid world as weaker competition dies out. Hopefully as the economy recovers from the Covid crisis, the performance of the portfolio should be markedly different than what we have seen in the last three years, an era of high risk taking and limited focus on downside risk.

Q2. The Fund you co-manage - Quantum Long Term Equity Value Fund, is founded on these same value principles? How has this approach panned out for you?

We had a fantastic run in the first 10 years (200--2016), where we were much ahead of the benchmark despite significant underperformance between 2006-2008. Last three years have been tough for us as markets rallied despite very weak economic fundamentals, driven by a handful of stocks. Too much liquidity sloshing around as evidenced by low interest rates and investors seeking to pile into stocks that have already risen by 100% assuming risks are non-existent, is not the environment where value investing will do well. At such times the portfolio team waits patiently for froth to disappear as corrections can be quite severe and can lead to significant erosion of capital.

We have seen such a cycle in 2007, that time it was the collapse of the US subprime market which triggered a correction. This time it is the Covid virus which triggered a similar correction. The portfolio team of the Quantum Long Term Equity Value Fund thrives under such circumstances. The sharp correction has allowed us to buy great businesses at valuations not seen since the crash of 2008. In between these large corrections there have been many mini hiccups or corrections which allowed our value style to flourish. These mini hiccup periods were those where risk was adequately accounted for.

One of our best periods has been post the 2008 crash where the quality of portfolio we had built gave a fantastic outperformance. Even though there are no guarantees, hopefully the portfolio we have built after the crash, allows us to get back to our long term outperformance levels. Once people start noticing the risks in equity investing our portfolio tends to do really well.

Q3. What's your advice to investors at this point in time? For both...those who are looking to get in, and those, who are seasoned investors?

India remains a fantastic long term compounding story. However, the sharp rally over the last three months', despite the very weak economic activity, has made risk - reward slightly unfavorable for investors looking to make large lump sums of investments. SIP remains the best way to allocate funds over long periods of time because of its feature to average investment costs. For investors looking to make large lump sum allocation perhaps investing 75% now and the balance 25% if the markets were to sell off may be a much better strategy.

Q4. How do you see the Indian economy pan out in the months to come? How do you think this will impact the performance of your Quantum Long Term Equity Fund in the near future?

The economy which was not in the best shape even before Covid has been dealt another significant blow, recovery for which is expected to be gradual. It's likely that corporate earnings over FY20-22 post zero growth with a possible downside risk. We expect companies to get back to some normalcy in FY22 and for the process of economic expansion to resume.

Traditionally, we have seen the value style do really well during phases of economic turns as valuation normalization is sharper or companies trade at a deep discount to their fair value. Hopefully as things normalize in FY22 we should have a similar effect on the performance of the fund

Q5. Black swan events do happen. In recent times, we have seen the Great Financial Crisis, and now, Covid-19. How have you navigated such events? How did this pan out in terms of end returns?

There were essentially two major corrections that unfolded in the market after the fund was launched (this is before the Covid related correction). First was the Global financial crisis in 2008 which was triggered after a meltdown in US subprime markets. This came at the back of one of the biggest rally's equity markets had seen globally and investors had forgotten equity investing also involved significant downside risks. Before the correction it was not the best of times for us as we sounded caution at a time of extreme exuberance. Our performance lagged as we were buying companies which were not taking undue risks while the market preferred otherwise.

It was only after the crash that our portfolio shone through. Investors liked the sensible nature of the businesses we owned with very little balance sheet risks The second major correction was the taper tantrum in 2013, when US fed governor Ben Bernanke hinted for the first time that they may be raising interest rates. Investors who used to price assets assuming very low interest rates were in for a shock. 2014-2016 was also quite good for us as the quality of the portfolio again helped us navigate a stressful period. The Covid crash is different in the sense that the Indian economy is much more impacted this time than in the previous two events We have traditionally built a portfolio of quality businesses with very low balance sheet risk, at comfortable valuations and this time it's no different. Hopefully this crash proves more of the same and we bounce back strongly.

Editor's Note: Want to learn more about why investing in Value funds makes sense for your overall portfolio. Write to us at [email protected] Or give us a missed call at +91-22-68293807 and we will call you back.

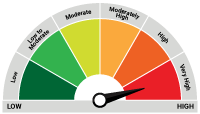

| Name of the Scheme & Primary Benchmark | This product is suitable for investors who are seeking* | Risk-o-meter of Scheme |

| Quantum Long Term Equity Value Fund An Open Ended Equity Scheme following a Value Investment Strategy | • Long term capital appreciation • Invests primarily in equity and equity related securities of companies in S&P BSE 200 index. |  Investors understand that their principal will be at Moderate Risk |

* Investors should consult their financial advisers if in doubt about whether the product is suitable for them.

Disclaimer, Statutory Details & Risk Factors:

The views expressed here in this article / video are for general information and reading purpose only and do not constitute any guidelines and recommendations on any course of action to be followed by the reader. Quantum AMC / Quantum Mutual Fund is not guaranteeing / offering / communicating any indicative yield on investments made in the scheme(s). The views are not meant to serve as a professional guide / investment advice / intended to be an offer or solicitation for the purchase or sale of any financial product or instrument or mutual fund units for the reader. The article has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. Whilst no action has been solicited based upon the information provided herein, due care has been taken to ensure that the facts are accurate and views given are fair and reasonable as on date. Readers of this article should rely on information/data arising out of their own investigations and advised to seek independent professional advice and arrive at an informed decision before making any investments. Please visit – www.quantumamc.com/disclaimer to read scheme specific risk factors.

View All

Related Posts

-

The Index of Services Production

Posted On Tuesday, Jul 28, 2026

Every month, India publishes a number for how much steel, cement, and electricity the economy produced via IIP (Index of Industrial Production).

Read More -

Equity Outlook - July 2026

Posted On Wednesday, Jul 01, 2026

Indian equities recovered in the month of June, as the West Asia crisis showed signs of de-escalation.

Read More -

Debt Outlook - July 2026

Posted On Wednesday, Jul 01, 2026

The Indian fixed income market enters the second half of FY27 with a macro backdrop that is becoming increasingly supportive for bonds, even as inflation risks remain on the horizon.

Read More