Smart Investing: Pre-Investment Checklist for Debt Mutual Funds

Posted On Thursday, Apr 11, 2019

Recent events involving delay and deferment of redemptions proceeds of Fixed Maturity Plans of some fund houses due to the apparent delay in payments by Essel Group companies has reignited the issue of risks in debt funds. As we have been maintaining, that the credit crisis in the bond markets which began in September 2018 is not over yet and investors should prioritize Safety and Liquidity over Returns while investing in debt funds.

Over the last 5 years, there have been many events of defaults in debt mutual funds and some of which have happened in Liquid Funds, wherein the investor is completely not prepared to accept credit risks and defaults.

Debt Fund investing is thus often mis-construed and leaves many investors with dissonance. But If invested carefully by keeping your objective simple and clear, Debt Funds can be a good portfolio diversification tool which can give returns, with lower volatility than equities and with some tax benefits over fixed deposits.

The investors should keep in mind the following tenets while investing in Debt funds

- Debt Funds/ Bond Funds are NOT wealth generating products. Do not expect and try to earn fabulous returns from this product. They are meant to provide returns around what you earn similar in bank deposits subject to market risks and in some cases have better taxability over fixed deposits

- Debt Funds can be considered as an alternate option to your existing debt/fixed income investments – Do know that you already have enough money lying in bank savings, deposits, company PF, PPF, endowment insurance.. These are all fixed income investments and Debt mutual funds then should only act as a substitute/alternate to the other investment options depending on liquidity, maturity, and return expectation. Therefore, many would find that they actually don’t need any more fixed income exposure and may need to allocate more to equities.

- Debt Funds are NOT Bank Fixed Deposits. Even Fixed Maturity Plans are NOT Bank Fixed Deposits. The returns from a Debt Fund are not guaranteed under any circumstance, including in FMPs, as investors have now found out.

- Debt Funds carry

- Market risks: change in NAV due to change in the prices of the bonds it holds – : happens very frequently as market interest rates change based on changes in the macro environment. Longer tenor bonds are more sensitive to interest rate changes and bond funds which invest in those securities carry higher market risks.

- Credit Risks: fall in NAV due to deteriorating financial/governance profile of the company in which the fund is invested resulting in credit rating downgrades resulting in higher bond yields and lower bond prices. If this results in a contagion, then bond prices of good companies also get impacted - Recent example – Dewan Housing scare resulting in rising yields of all NBFCs

- Default Risks: fall in NAV due to non-payment of interest and/or principal by the corporate; Recent Eg- ILFS and its subsidiaries

- Liquidity Risks: Inability of the fund to sell its investments and meet redemptions of investors due to poor market conditions. Recent eg: in an event of a credit crisis, the sentiment sours and demand for low quality credit papers drop. Thus funds may not be able to sell investments even if they sense trouble.

- Debt Funds may require longer time holding periods in order to play out a cycle and also to benefit from the long term capital gains taxation which kicks in after holding period of 3 years.

Debt funds can be classified under 4 broad categories – Liquid and Money Market, Short term, Dynamic/Long Term, Credit Risk Funds.

Liquid Funds – Have low market risks, but as events of the last 4 years suggests, it can have Credit and Default risks. Liquid Funds/Money Market Funds are meant to invest your short term cash surplus. We see no reason whatsoever in taking credit risks and trying to earn higher returns in this segment of your allocation. Choose Liquid Funds which avoid credit risks.

Short Term Bond Funds - Has higher market risks than Liquid And Money Market funds. This segment generally considered as an alternate option to 1-3 year fixed deposits. So, evaluate between them depending on the pointers mentioned above, especially on the extent of credit risks the fund carries in its portfolio.

Fixed Maturity Plans (FMPs) also tend to be in the 1-3 year category. But FMPs are close ended and investors at most time have to remain fully invested till maturity. FMP portfolios tend to be concentrated and hence should also be closely evaluated on the credit risks, as the recent event has outlined.

Long Term/ Dynamic Bond Fund - Can have very high market risks and is the segment where investors tend to grapple most on the distinction between the aspect of fixed income and volatility in the NAV and returns. Bond Funds often have periods of low and/or negative returns which investors are not prepared for and hence we mention that investors may need to hold it for a longer period for the interest rate cycle to play out. Investing in a Dynamic Bond Fund, which allows the fund manager flexibility to manage the interest rate risk is a better option. We would also recommend to choose Dynamic Bond Funds which take lower credit risks and have a liquid portfolio.

Credit Risk Funds – We genuinely believe that retail investors should stay away or if at all allocate a very small portion of their investment in this category. The Indian bond market at the current state of its development in this category still remains illiquid and mis-priced. This product is only for sophisticated and High Net worth investors. So, if while investing in bond funds for generating fixed income, you are not prepared to absorb any of these risks, then you are better off investing in safe bank deposits.

Quantum Liquid Fund prioritizes safety and liquidity over returns as its investment objective. Quantum Liquid Fund does not invest in any Private Corporate Debt instruments thus minimizing the credit risk. The Returns of the Quantum Liquid Fund may be lower than peers but it also takes lesser risks.

Quantum Dynamic Bond Fund takes market risks but runs a liquid portfolio by investing only in government securities, state government securities and AAA/A1+ PSU instruments.

We disclose our portfolios of Quantum Liquid Fund and Quantum Dynamic Bond Fund on a weekly basis enhancing transparency.

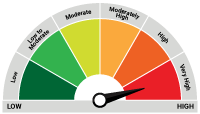

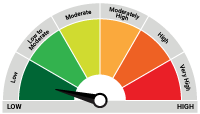

| Name of the Scheme & Primary Benchmark | This product is suitable for investors who are seeking* | Risk-o-meter of Scheme |

| Quantum Dynamic Bond Fund An Open Ended Dynamic Debt Scheme Investing Across Duration | • Regular income over short to medium term and capital appreciation • Investment in Debt / Money Market Instruments / Government Securities. |  Investors understand that their principal will be at Moderate Risk |

| Quantum Liquid Fund An Open Ended Liquid Scheme | • Income over the short term • Investments in debt / money market instruments. |  Investors understand that their principal will be at Low Risk |

* Investors should consult their financial advisers if in doubt about whether the product is suitable for them.

Disclaimer, Statutory Details & Risk Factors:

The views expressed here in this article / video are for general information and reading purpose only and do not constitute any guidelines and recommendations on any course of action to be followed by the reader. Quantum AMC / Quantum Mutual Fund is not guaranteeing / offering / communicating any indicative yield on investments made in the scheme(s). The views are not meant to serve as a professional guide / investment advice / intended to be an offer or solicitation for the purchase or sale of any financial product or instrument or mutual fund units for the reader. The article has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. Whilst no action has been solicited based upon the information provided herein, due care has been taken to ensure that the facts are accurate and views given are fair and reasonable as on date. Readers of this article should rely on information/data arising out of their own investigations and advised to seek independent professional advice and arrive at an informed decision before making any investments. Please visit – www.quantumamc.com/disclaimer to read scheme specific risk factors.

View All

Related Posts

-

The Index of Services Production

Posted On Tuesday, Jul 28, 2026

Every month, India publishes a number for how much steel, cement, and electricity the economy produced via IIP (Index of Industrial Production).

Read More -

Equity Outlook - July 2026

Posted On Wednesday, Jul 01, 2026

Indian equities recovered in the month of June, as the West Asia crisis showed signs of de-escalation.

Read More -

Debt Outlook - July 2026

Posted On Wednesday, Jul 01, 2026

The Indian fixed income market enters the second half of FY27 with a macro backdrop that is becoming increasingly supportive for bonds, even as inflation risks remain on the horizon.

Read More