Plan Your Retirement in Advance to Secure Your Future

Posted On Wednesday, May 18, 2016

Everyone generally loves living long. Try asking someone who just celebrated their 70th birthday, in case this sounds skeptical! ?

Like the old internet joke comparing human life span with animals goes, for the first 20 years of our life we eat, sleep, play, and enjoy ourselves. For the next 40 years we slave in the sun like a cow does, to support our family. For the next 10 years we do monkey tricks to entertain the grandchildren. And for the last 10 years we sit on the front porch like cats do and watch others go by their lives! Old age is supposed to be that part of one’s life which is care-free, spending time with the grandchildren, doing things one always dreamed of in their hurry-worry-filled work phase.

However sadly for an alarming proportion of India’s population, retirement and old age is far, far away from the bliss and happiness everyone hopes for in this phase.

Retirement – not so golden for many

Various studies based on the last national census (2011) suggest that about 60-70% of the aged in the country had to depend on others for their day-to-day maintenance. The others here being the children chiefly; spouses, grandchildren and sometimes even non-relations included. (Source: Mospi) Moreover, of those who had the fortune of being economically independent, 90% had to support one or more dependents.

In keeping with the global trend, life expectancy of India has been rising over the years. It was around 66 years in 2010, and retirement age varies in different sectors, ranging from 52 years to 65 years. But this blessing of rising life expectancy translates to another unfortunate trend: the proportion of the oldest elderly (aged 80 years and above) among the working population is relatively high in India compared to many other countries. A majority of the elderly work due to economic necessity and not out of choice or chance. And of course a majority of these elderly workers are self-employed because employers do not prefer them due to their declining state of health and energy.

No pension for 9 out 10 elderly!

Why is the vast majority of the aged population economically dependent? The straightforward reason is that, barring a few fortunate seniors who have pension, the rest has neither pension nor savings of their own. Figures point out that only about 8-15% senior citizens, most of who have been in government service are entitled to pension. This means that roughly 9 out of every 10 non-working senior citizen in the country gets no pension. The statistics is better for retirees in the urban areas but only slightly; about 16% senior citizens get pension compared to 10% in the rural areas, according to a UNFPA report.

Actually it is not a surprise that so few senior citizens earn pension. The scope of pension is seemingly limited to government jobs alone. Private sector employees in the organized sector have the Employee Provident Fund (EPF). However the organized sector represents only about 10% of India’s total working population. The overwhelming majority of the aged Indians has been employed in the non-organized sector, where employment conditions are poor and is reflecting in pitiable post-retirement benefits.

Where am I?

The fact and figures above brings us to stop and think on where we are on our own journey to retirement. Now most of us dislike thinking of ageing, forget preparing for it… but the good part is with a little bit of planning and effort retirement could be an extended holiday that we actually look forward to ?

For starters you can get an approximate idea of how much a comfortable retirement would cost by punching in a few numbers on our Retirement Calculator. Just to throw in a rough idea; if you are in your 30`s and presently live on a modest Rs 2.5 lakhs budget per annum (EMI`s excluded) then this would transform to somewhere close to Rs 1 crore per annum by the time you retire after 30 years!

Those of us employed in the private sector would have to patiently build the old age nest egg by ourselves. But this could be a blessing in disguise as we have the liberty to invest our savings wisely rather than being compelled to park retirement savings in fixed income financial products whose yields are comparatively lower than growth assets. As for those employed in the government sector that may have some form of pension to fall back on during their golden years, in all likelihood such pension alone would barely be sufficient to see them through. They too would have to invest for building a sufficient retirement corpus.

Give yourself a generous retirement income source

Now regardless of which group of the two you belong to, you can confidently aim at gifting yourself a generous self-made pension by investing systematically in mutual funds. Here is a suggested investment guide for building your retirement corpus with mutual funds.

| Years to retire | Suggested investment |

| 5-7 years or more | An equity funds combo of Quantum Long Term Equity Fund & Quantum Equity Fund of Funds |

| Less than 5-7 years | Quantum Multi Asset Fund |

Quantum Long Term Equity Fund (QLTEF) is our flagship fund which offers a solid, research based portfolio suitable for long term investments. Quantum Equity Fund of Funds (QEFOF) is a fund which invests in 5-7 suitable equity funds managed by other AMCs. QLTEF and the funds in QEFOF can perform differently in different market cycles as their mandates and fund management styles vary. Therefore while we encourage investors to confidently invest some amount of their savings in QLTEF we also advocate that some portion of their equity funds allocation should be in a fund like QEFOF. Together these 2 funds give you a robust, diversified portfolio for building your long term retirement corpus.

Quantum Multi Asset Fund (QMAF) on the other hand is suitable for investors who are close to their golden years. Whatever corpus has been accumulated through the years can be parked in this fund whose portfolio is spread across equities, debt and gold. So your portfolio gets the balance of a growth edge with equities and also the stability of fixed income and gold.

But the important key here is to start as early as possible. For an illustration, suppose that at 30 years of age you begin building the corpus with a monthly allocation of Rs 5,000 earning a 12% yearly return, at 60 years you would have accumulated about Rs 1.77 crores. What if you delay by just 2 years? Your corpus would be short of almost Rs 39 lakhs; i.e. your end corpus would be around Rs 1.38 crores. Please key in the numbers in our SIP calculator to understand this better.

Mutual funds offer a standardized option for making monthly investments in any given fund and this is called by the name SIP or Systematic Investment Plan. Start an SIP as suggested in the table above and consider retirement investment as a mandatory personal PF deduction! But remember that ultimately your choice of investment would depend on factors such your risk appetite (which is a function of your age to an extent) and asset allocation needs. Hence also consult with your financial advisor on the most suitable choices for your goal.

If you’d like to know more about Quantum, our funds or would like assistance on starting your investments, do write to us on [email protected] or give us a missed call on 9243223863. We will be glad to assist.

Product Labeling

| Name of the Scheme & Primary Benchmark | This product is suitable for investors who are seeking* | Risk-o-meter of Scheme |

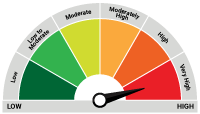

| Quantum Long Term Equity Value Fund An Open Ended Equity Scheme following a Value Investment Strategy | • Long term capital appreciation • Invests primarily in equity and equity related securities of companies in S&P BSE 200 index. |  Investors understand that their principal will be at Moderate Risk |

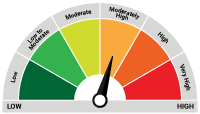

| Quantum Equity Fund of Funds An Open Ended Fund of Funds scheme Investing in Open Ended Diversified Equity Schemes of Mutual Funds | • Long term capital appreciation • Investments in portfolio of open-ended diversified equity schemes of mutual funds registered with SEBI whose underlying investments are in equity and equity related securities of diversified companies | Investors understand that their principal will be at Very High Risk |

| Quantum Multi Asset Fund of Funds (An Open Ended Fund of Funds Scheme Investing in schemes of Quantum Mutual Fund) | • Long term capital appreciation and current income • Investments in portfolio of schemes of Quantum Mutual Fund whose underlying investments are in equity , debt / money market instruments and gold |  Investors understand that their principal will be at Moderately High Risk< |

* Investors should consult their financial advisers if in doubt about whether the product is suitable for them.

Disclaimer, Statutory Details & Risk Factors:

The views expressed here in this article / video are for general information and reading purpose only and do not constitute any guidelines and recommendations on any course of action to be followed by the reader. Quantum AMC / Quantum Mutual Fund is not guaranteeing / offering / communicating any indicative yield on investments made in the scheme(s). The views are not meant to serve as a professional guide / investment advice / intended to be an offer or solicitation for the purchase or sale of any financial product or instrument or mutual fund units for the reader. The article has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. Whilst no action has been solicited based upon the information provided herein, due care has been taken to ensure that the facts are accurate and views given are fair and reasonable as on date. Readers of this article should rely on information/data arising out of their own investigations and advised to seek independent professional advice and arrive at an informed decision before making any investments. Please visit – www.quantumamc.com/disclaimer to read scheme specific risk factors.

View All

Related Posts

-

The Index of Services Production

Posted On Tuesday, Jul 28, 2026

Every month, India publishes a number for how much steel, cement, and electricity the economy produced via IIP (Index of Industrial Production).

Read More -

Equity Outlook - July 2026

Posted On Wednesday, Jul 01, 2026

Indian equities recovered in the month of June, as the West Asia crisis showed signs of de-escalation.

Read More -

Debt Outlook - July 2026

Posted On Wednesday, Jul 01, 2026

The Indian fixed income market enters the second half of FY27 with a macro backdrop that is becoming increasingly supportive for bonds, even as inflation risks remain on the horizon.

Read More