The Liquidity Glut

Posted On Monday, Dec 14, 2020

Liquidity is the life blood of an economy. For a smooth functioning of any economy, it is essential to have adequate levels of liquidity flowing in the system. Its role becomes even more important in times of economic crisis, like the one we are facing now.

Easy liquidity conditions in the banking and financial markets facilitate flow of credit to the broader economy. It reduces cost of funds and thus helps in increasing demand. More than anything, it fuels a risk taking sentiment among investors and other economic agents.

Central banks create excess liquidity to deal with a crisis. They did so post the Great Financial Crisis (GFC) of 2008. They have again resorted to using various tools to create more and more liquidity to deal with the economic collapse caused by the corona virus (or COVID-19).

It hasn't been any different in India. The RBI has also been creating money and pumping liquidity into the banking system.

The RBI usually creates money and adds rupee liquidity by buying government bonds or buying dollars. Over the last 2 years, it has added liquidity by buying government bonds in what is known as Open Market Operations. It has also 'intervened' in the FX market by buying up the dollar inflows. The RBI has emerged as a large player in both the bond and the currency markets. The trajectory of bond yields and the value of INR depends heavily on what the RBI does on liquidity.

Capital flows and FX interventions

Liquidity addition was not the only motive of its intervention in the bond and FX markets. It was rather a consequence of RBI's efforts to keep bond yields low to support growth and help fund the government's fiscal deficit. Since November 2018, the RBI has bought Rs. 5.9 trillion worth of government bonds, which is about 43% of the net central government borrowing in this period.

The FX intervention was to protect INR from appreciating in the face of large foreign capital inflows. Foreign portfolio investors infused over USD 20 billion into Indian markets from April-November 2020, mainly into the equity markets. Another USD 22 billion came in in the form of Foreign Direct investments between April-September 2020 (last reported till September). Capital inflows from foreign sources is good news. But a sudden sizeable inflows of foreign currency causes value of INR to appreciate and in turn can make our exports less price competitive.

In order to avoid any large appreciation in INR, the RBI bought most of these inflows. Its foreign exchange reserves swelled from USD 475 billion in March 2020 to USD 575 billion in November 2020. This, in turn, added about Rs. 5 trillion of additional rupee liquidity into the banking system.

The RBI has also been innovative

Apart from the usual, RBI has used multiple and often innovative ways to create liquidity. It introduced forex swaps, LTROs (long term repo operations) and Targeted LTROs (T-LTRO). It also reduced the CRR (Cash Reserve Ratio) for banks for the first time in 7 years.

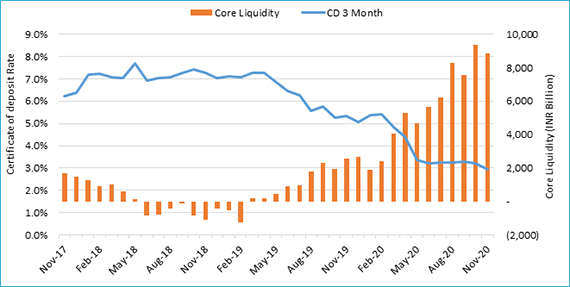

Banks are currently parking around Rs. 6.5 trillion with the RBI on daily basis under its reverse repo window. Moreover, the central government is sitting on an unspent surplus balance of about Rs. 2.5 trillion. This will also find its way into the banking system at some point when government start spending. The Core liquidity which includes unspent government balances is about Rs. 8 trillion.

The liquidity in stealth and the subtle innovations has worked. Overnight and short term rates have fallen way more than the actual reduction in the Repo and Reverse Repo Rates. The fact that even commercial paper rates are down suggests that the excess liquidity has also lowered risk aversion to an extent.

The Trade-off

With sharp increase in liquidity surplus in October and November, money market rates collapsed to decadal lows, well below the 'perceived floor' - the reverse repo rate. As of November 30, 2020 the overnight tri-party repo rate (collateralized lending & borrowing) was about 2.9% as against reverse repo rate of 3.35%. Even yields on short term commercial papers of public sector companies were quoting below 3.0%.

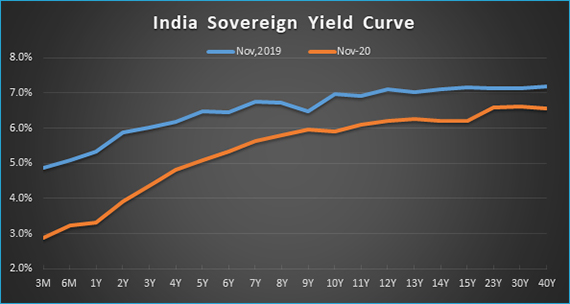

But as they say, "you can't have it all". As the RBI's forex interventions increased in the last two months, it turned hesitant in conducting bond (OMO) purchases.

In its October 2020 monetary policy, the RBI had committed to conduct OMO purchases worth Rs. 200 billion every week. Not wanting to add liquidity, the RBI has not bought any government bond in the last three weeks. Prior to that they had replaced outright OMOs with operation twists (an innovation where they buy long term bonds and sell short term bond) but for a lesser amount. This is to keep liquidity neutral but yet manage bond yields.

Absence of RBI buying has now started putting upward pressure on long term bond yields. The yield curve which was already very steep, has become even steeper.

The other side

Although easy liquidity is essential for the economy to come out of this slump, there are side-effects of too much liquidity which cannot be ignored. In India, our past experiences with high liquidity surpluses to boost growth have not been pleasant.

Liquidity infused during the 2008 global financial crisis led to out of control inflation in the subsequent period. It ended up badly in 2013 when India was termed a part of 'fragile five' - group of economies at cusp of collapse. The economy suffered badly and the Indian Rupee took a heavy beating.

Most recent experience with excess liquidity during the demonetization was also not comforting. High liquidity and low short term rates fueled excessive risk taking especially among the non-bank finance companies (NBFCs). Many of them started borrowing too much through short term bonds to fund their long term assets growth. Investors found it as an easy way to earn extra returns over fallen bank deposit rates. Ultimately, this bubble burst in 2018 when the IL&FS failed to roll over its ballooning debt. Economy is yet to recover from that shock and many debt fund investors have still not been able to recoup their losses.

Outlook

Going into the December monetary policy, there was an expectation that the RBI will announce measures to take out excess liquidity. Contrary to this belief, the RBI didn't show any worry on the prevailing liquidity situation. We see it as a wait and watch stance from the RBI.

Central banks in industrial countries have committed to keep interest rates near zero and keep the liquidity flowing for long period of time. The developed world has been dealing with this problem of too much money and too little yield for many years. If the global liquidity situation persists and risk appetite increases with vaccine and economic recovery, flows to emerging economies like India can increase substantially.

If so happens, the RBI will be forced to devise ways to absorb liquidity from the banking system or they will have to leave either the INR or bond yields to find their own equilibrium. What complicates the matter even further is the inflation. If inflation remains high, keeping liquidity in large surplus and short term interest rates below reverse repo will become challenging for the RBI.

However like many other central banks, the RBI is also ready to tolerate slightly higher inflation for some time and focus on reviving the economy. Given the economic recovery is still at a nascent stage, the RBI will likely maintain the current low rates and excess liquidity for an extended period. Its interventions in the currency and the bond markets may also continue.

Portfolio Positioning - Tactical vs Structural Trade

In the Quantum Dynamic Bond Fund (QDBF) portfolio we continue to focus on tactical trading opportunities within a narrow range. QDBF does not take any credit risks and invests only in sovereigns and top-rated PSU bonds, but it does take high-interest rate risk from time to time.

Given the yield curve is already very steep and the RBI is actively intervening in the market to protect long bond yields from rising, we are positioned at the longer end of the maturity curve which is offering better accrual yield.

This is a tactical position that can change based on market developments and new information flows. Given the objective of our fund stated in the name itself - we retain our right to remain dynamic in our portfolio construction as we remain cognizant of these risks on the horizon.

We understand the economy and markets are currently adjusting to an unprecedented shock. There are too many moving parts and things are still evolving. Thus, any forecast about the future is susceptible to change based on policy responses from the government and the RBI and the changes in global markets. We stand vigilant to review our outlook as and when new information comes. Nevertheless, it would be prudent for investors to be conservative at times of heightened uncertainty.

Investors should lower their return expectations from fixed income - as money market yields, fixed deposits will remain low, and potential capital gains from long bond funds will be muted.

Credit Crisis is not over yet

We reiterate our view that the credit crisis in the bond market is not over yet. The Indian economy has faced a severe jolt due to a national lockdown. This has significantly weakened the debt servicing capacity of many companies and individuals. This could create a negative spiral in the economy and hence in the loan and bond markets. We see a high risk of rating downgrades and defaults in the next two years.

In this scenario, it would be prudent for investors to avoid excessive credit risk in their debt exposure.

Source : RBI, Bloomberg

For any further queries you can write to us at

[email protected] / [email protected] or call us on Tel: 9870458160 / 8689961495

| Name of the Scheme | This product is suitable for investors who are seeking* | Riskometer |

| Quantum Dynamic Bond Fund An Open Ended Dynamic Debt Scheme Investing Across Duration | • Regular income over short to medium term and capital appreciation • Investment in Debt / Money Market Instruments / Government Securities |  |

Disclaimer, Statutory Details & Risk Factors:

The views expressed here in this article / video are for general information and reading purpose only and do not constitute any guidelines and recommendations on any course of action to be followed by the reader. Quantum AMC / Quantum Mutual Fund is not guaranteeing / offering / communicating any indicative yield on investments made in the scheme(s). The views are not meant to serve as a professional guide / investment advice / intended to be an offer or solicitation for the purchase or sale of any financial product or instrument or mutual fund units for the reader. The article has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. Whilst no action has been solicited based upon the information provided herein, due care has been taken to ensure that the facts are accurate and views given are fair and reasonable as on date. Readers of this article should rely on information/data arising out of their own investigations and advised to seek independent professional advice and arrive at an informed decision before making any investments.

Mutual fund investments are subject to market risks read all scheme related documents carefully.

Please visit – www.QuantumAMC.com to read scheme specific risk factors. Investors in the Scheme(s) are not being offered a guaranteed or assured rate of return and there can be no assurance that the schemes objective will be achieved and the NAV of the scheme(s) may go up and down depending upon the factors and forces affecting securities market. Investment in mutual fund units involves investment risk such as trading volumes, settlement risk, liquidity risk, default risk including possible loss of capital. Past performance of the sponsor / AMC / Mutual Fund does not indicate the future performance of the Scheme(s). Statutory Details: Quantum Mutual Fund (the Fund) has been constituted as a Trust under the Indian Trusts Act, 1882. Sponsor: Quantum Advisors Private Limited. (liability of Sponsor limited to Rs. 1,00,000/-) Trustee: Quantum Trustee Company Private Limited. Investment Manager: Quantum Asset Management Company Private Limited. The Sponsor, Trustee and Investment Manager are incorporated under the Companies Act, 1956.

View All

Related Posts

-

Debt Outlook - August 2026

Posted On Monday, Aug 03, 2026

Indian fixed income enters August after its sharpest single-week scare of an already volatile quarter.

Read More -

Equity Outlook - August 2026

Posted On Monday, Aug 03, 2026

Indian equities were flat in the month of July, as the West Asia crisis re-escalated. Flair up in the West Asia conflict resulted in crude

Read More -

Gold Outlook - August 2026

Posted On Monday, Aug 03, 2026

After falling sharply in June, July has brought in some stabilisation for gold. The metal recovered toward

Read More