FCNR 2.0: Same Instrument, Different India Why 2026 Is Not 2013

Posted On Friday, Jun 19, 2026

When the Reserve Bank of India (RBI) announced a fresh FCNR(B) mobilization scheme and concessional swap facility in its June 2026 monetary policy, markets immediately drew parallels with September 2013.

The comparison is understandable.

The last time this toolkit was deployed, India was at the center of the "Fragile Five" episode, alongside Brazil, Indonesia, South Africa and Turkey. A sharply depreciating rupee, record current account deficits and deteriorating investor confidence had placed significant pressure on India's external balance sheet.

The FCNR(B) programme introduced under Governor Raghuram Rajan eventually mobilized nearly USD 34 billion, helping stabilize the rupee and restore confidence in India's external position.

Yet viewing 2026 as a replay of 2013 misses the bigger story.

The instrument may be the same, but the macroeconomic backdrop is fundamentally different.

In 2013, India needed dollars. In 2026, it is seeking to strengthen an already robust external position while improving domestic liquidity and lowering the economy's cost of capital. With foreign exchange reserves above USD 680 billion, a manageable current account deficit and stronger financial-sector fundamentals, this looks less like a crisis-response measure and more like a proactive balance-sheet optimization exercise.

India's ability to mobilize overseas capital through its diaspora is not new.

From India Development Bonds in 1991 and Resurgent India Bonds in 1998 to India Millennium Deposits in 2000 and the FCNR(B) scheme in 2013, policymakers have repeatedly leveraged a unique structural advantage: access to a large and globally diversified NRI investor base. What makes the 2026 programme particularly noteworthy is that it has been launched in the absence of an actual external funding crisis.

At its core, FCNR(B) is a mechanism for importing dollar liquidity into the Indian banking system. NRIs place foreign currency deposits with Indian banks, earning dollar-denominated returns while remaining insulated from rupee depreciation. Banks gain access to foreign currency funding and India benefits from an inflow of stable external capital.

The success of the 2013 programme stemmed from the RBI's concessional swap facility, which significantly reduced hedging costs and made participation attractive.

The 2026 framework goes a step further, with more supportive terms on hedging, broader eligibility and the potential use of leverage, raising the possibility that inflows could match or may be even exceed the levels achieved in 2013.

To understand why, it is worth revisiting the circumstances that made the original FCNR(B) programme so effective.

Chapter One: When India Was One of the Fragile Five

To appreciate the significance of the 2013 FCNR(B) programme, it is worth remembering how vulnerable India appeared at the time.

The current account deficit had widened to a record 4.8% of GDP. Inflation remained elevated, fiscal deficits were large and the economy had become increasingly dependent on foreign capital to finance its external imbalance.

What appeared manageable in a world awash with liquidity suddenly became far more precarious when global conditions began to change and that change arrived in May 2013…

When Federal Reserve Chairman Ben Bernanke first hinted at tapering quantitative easing, investors rapidly reassessed emerging-market risk. The resulting "Taper Tantrum" triggered a broad flight of capital from developing economies. Currencies weakened, bond yields rose and countries with large external financing requirements found themselves under intense scrutiny.

And India was among the most exposed economies…

The rupee depreciated from around ₹55 per dollar to nearly ₹69 within months. Foreign investors reduced exposure, sovereign risk premia widened and India was grouped alongside Brazil, Turkey, South Africa and Indonesia in the now infamous "Fragile Five" basket.

Chart I: Amid the 2013 "Fragile Five" turmoil, the INR fell nearly 28% from peak to trough in just four months, leading the RBI to raise policy rates and launch the FCNR(B) and ECB schemes

and ECB schemes")

Data Source: LSEG, DataStream. Quantum AMC Graphics. Above data represents respective currency’s values against USD rebased to 100. Data from December 31, 2011 to December 31, 2014. INR: Indian Rupee, IDR: Indonesian Rupiah, CNY: Chinese Yuan, BRL: Brazilian Real, ZAR: South African Rand, MX PESO: Mexican Peso

By mid-2013, the issue was no longer the rupee alone. Markets were beginning to question India's ability to finance its external deficit without a sharp adjustment in growth, imports or domestic liquidity.

It was against this backdrop that Raghuram Rajan assumed office as RBI Governor in September 2013.

What followed is often remembered as an FCNR(B) deposit mobilization programme. In reality, it was a broader confidence-restoration exercise.

FCNR(B) deposits already existed. Rajan's innovation was to transform the incentives surrounding them. Banks were allowed to swap NRI dollar deposits with the RBI at a fixed concessional rate of 3.5%, while selected overseas borrowing restrictions were relaxed.

The economics became compelling. Banks could offer attractive returns without bearing the full hedging cost. Investors gained access to yield at a near-zero interest-rate . India gained a rapid source of stable foreign currency funding.

Equally important, the programme changed the market psychology.

At a time when confidence was fading , the RBI demonstrated that it had both the policy flexibility and institutional credibility to mobilize capital at scale.

The signal mattered almost as much as the dollars themselves.

Within months, FCNR(B) deposits and related overseas borrowings mobilized nearly USD 34 billion. The rupee stabilized, reserves increased, balance-of-payments concerns receded and sovereign risk premia compressed.

Chart II: During the FCNR(B) swap window from September to December 2013, approximately USD 24.5 billion was mobilized.

swap window from September to December 2013, approximately USD 24.5 billion was mobilized.")

Data Source: Source: RBI.

Rajan's intervention succeeded not because it directly defended the currency, but because it restored confidence in India's external balance sheet.

That distinction is important when evaluating the RBI's decision to revisit the same approach in 2026.

Chapter Two: From Fragile Five to Global Growth Engine

The most important difference between 2013 and 2026 is not the policy.

It is India's starting point.

In 2013, investors worried about India's external vulnerability. In 2026, India enters this phase with foreign exchange reserves exceeding USD 680 billion, a manageable current account deficit, stronger banking-sector fundamentals and increasing integration into global debt markets.

Over the past decade, India's macroeconomic profile has undergone a significant re-rating.

The election of Prime Minister Narendra Modi in 2014 marked an important turning point in investor sentiment. While reforms evolved gradually over time, perceptions shifted materially. India strengthened its macroeconomic foundations, expanded digital infrastructure, deepened capital markets and improved policy credibility.

The cumulative result has been a transformation in how investors view the country.

India is no longer seen primarily through the lens of vulnerability.

It is increasingly viewed through the lens of opportunity.

Table I Between 2013 and 2026, India’s macro story has moved decisively from fragility concerns to a sustained re-rating of its external and institutional strength

Data Source: CMIE. CMIE, RBI, Bloomberg, MoSPI. * Data as at the end of the respective FY # INR/$ currency fluctuation is calculated on a financial year YOY basis. Above inflation figures from FY23 onwards are as per the revised base of 2023-24.

Four Reasons 2026 Is Not 2013

1) India Is Not Fighting a Crisis

The 2013 programme was designed because India needed dollars.

The 2026 programme appears to be designed because the RBI would prefer to have more dollars.

That distinction is critical.

India today has one of the largest reserve buffers in the emerging-market universe. External vulnerability indicators are materially stronger, reserve adequacy metrics remain comfortable and the current account deficit appears manageable.

This looks less like a rescue measure and more like a precautionary step.

Table II: What was once a crisis-response framework has, in 2026, evolved into a tool of macro-financial optimization.

Data Source: Trading Economics. Data up to year ended March 2026. *Turkey's numbers require caution because reserve accounting, swaps and net reserve metrics have changed significantly over the period.

2) Global Capital Is More Expensive but the Economics are different

The arithmetic that powered the success of 2013 is considerably less favourable today.

In 2013, US interest rates were near zero, Treasury yields were historically low and dollar liquidity was abundant.

Today, investors can earn meaningful returns in US Treasuries, money-market funds and a wide range of alternative assets. The yield differential that once made FCNR deposits attractive has narrowed significantly.

Chart III: The Math Is No Longer As Compelling.

Data Source: Bloomberg. Quantum AMC graphics. UST refers to U.S. Treasury yields, and IGB refers to Indian Government Bond yields. The values shown in the boxes represent the yield differential (spread) between IGBs and USTs for the corresponding maturities for the respective years.

Participation can still be meaningful in 2026. But replicating the extraordinary scale of 2013 will be considerably more challenging.

While the interest-rate differential between India and the United States has narrowed materially over the past decade, the RBI has simultaneously improved the economics of participation for banks and depositors.

The comparison with 2013 is revealing.

Under the 2013 scheme, banks bore a concessional swap cost of 3.5% per annum. Under the 2026 framework, the RBI absorbs the entire hedge cost for FCNR(B) deposits. In effect, banks receive fully hedged foreign currency funding at no swap cost.

Deposits will also continue to be exempt from Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR) requirements, preserving the funding advantages that made the 2013 programme successful.

The new scheme also permits both fresh and renewal FCNR(B) deposits, unlike the 2013 programme which was limited to fresh mobilization. While this may slightly inflate headline flow numbers, it also broadens the potential pool of participation.

Furthermore, banks can now mobilize deposits with maturities ranging from three to five years, compared with the earlier requirement of three years and above.

Although the macro backdrop is less stressed than in 2013, the economics for banks may be better.

3) RBI Is Offering More Incentives

To compensate for a less favourable global environment, the RBI is shouldering a larger share of the burden.

By absorbing a substantial portion of the hedging cost, the central bank has improved the attractiveness of FCNR deposits. Deposit rates could potentially move into the 6%-7% range, creating a meaningful pickup in these instruments over comparable dollar instruments.

But an important innovation in the 2026 framework may not be the swap facility itself. It may be leverage…

The RBI has indicated openness to banks issuing Standby Letters of Credit (SBLCs) against FCNR deposits, enabling depositors to borrow against their capital and enhance returns. This substantially changes the investment proposition.

The leverage feature is arguably the single biggest reason why inflows in 2026 could potentially exceed those achieved in 2013 despite a less stressed macroeconomic environment.

The economics remain attractive.

The question is whether they are attractive enough to compete with the far broader investment universe available to global investors today.

4. Time Is Not On RBI's Side

The current mobilization window extends only until September 30, 2026.

Capital raising often depends on momentum. The shorter the window, the more important execution becomes.

Policy design matters.

But implementation matters just as much.

ECBs Have Been Expanded Significantly

The FCNR programme is only one half of the story.

The accompanying External Commercial Borrowing (ECB) framework has also been materially broadened.

Unlike the 2013 scheme, which was largely limited to banks and overseas borrowing facilities, the 2026 framework extends eligibility to Public Sector Undertakings (PSUs) and Authorized Dealer Category-I banks.

The coverage has also expanded to include ECBs, undrawn ECB lines and overseas foreign currency borrowings with maturities between three and five years.

Perhaps more importantly, the RBI has introduced a fixed swap cost of 1.5% per annum compared with the floating concessional framework used in 2013.

This certainty around hedging costs may improve execution and encourage broader participation.

Together, FCNR(B) deposits and ECB mobilization create a larger potential funding pool than was available thirteen years ago.

The Real Story Is Not the Rupee…

It Is the Cost of Capital

Much of the market discussion following the June 2026 announcement has focused on the rupee.

That is understandable.

FCNR(B) schemes are typically associated with foreign currency inflows, reserve accumulation and exchange-rate stability.

But the more important implication may be for India's cost of capital.

Alongside FCNR(B), the RBI has encouraged external commercial borrowings (ECBs), allowing banks, PSUs and quasi-sovereign institutions to access offshore funding easily.

This was an important, though often overlooked, feature of the 2013 programme.

Every dollar raised overseas is one less rupee that needs to be borrowed domestically.

When institutions such as SBI, REC, PFC, NABARD, EXIM Bank or IRFC access foreign capital markets, they compete less aggressively for domestic liquidity. Funding pressures ease, liquidity improves and borrowing costs decline across the fixed-income ecosystem.

The result is a two-fold benefit: stronger external balances and lower domestic funding pressure.

Both tend to support lower bond yields.

Chart IV: Government bond yields have softened across the curve since the policy announcement, with benchmark yields declining by around 15 bps, while the 15-year segment has outperformed, rallying nearly 41 bps.

Data Source: Bloomberg. Quantum AMC Graphics. Above data represent Indian Government bond yields in % terms as at the end of the previous month (May 29, 2026), RBI Monetary Policy Date (June 6, 2026) and Latest (June 15, 2026)

Why Corporate Bonds May Be (Use an alternative – avoid bigger winner)

Government bonds are usually the first market to react when external risks begin to recede. Lower currency risk, stronger reserves and improving liquidity conditions typically translate into lower sovereign yields.

But the more durable opportunity often emerges one step further down the transmission chain.

The significance of FCNR inflows, ECB mobilization and greater foreign participation is that they reduce the economy's overall cost of capital. As large borrowers gain access to offshore funding, pressure on domestic savings eases. Banks compete less aggressively for deposits, funding conditions improve and credit spreads begin to compress.

This process is already visible. CP and CD (Commercial Papers and Certificate of Deposits) rates have softened, corporate spreads have narrowed and demand for high-quality credit has strengthened.

Chart V: Since the policy announcement, AAA PSU bond yields have compressed by 12–23 basis points across the curve, with the strongest rally concentrated in the 3–5 year segment

Data Source: Bloomberg. Quantum AMC Graphics. Above data represents Corporate bond yields (for AAA PSU Nabard) in % terms as at the end of the previous month (May 29, 2026), RBI Monetary Policy Date (June 6, 2026) and Latest (June 15, 2026)

For borrowers such as PSUs, financial institutions and infrastructure-linked entities, this translates directly into a lower cost of capital. For investors, it highlights where the more compelling opportunity may lie. Government bonds may have led the rally, but the broad-based compression across the AAA corporate curve suggests that credit is increasingly becoming the second leg of the trade.

The benefits are unlikely to be distributed evenly. AAA-rated PSU issuers, financial institutions and infrastructure-linked borrowers appear particularly well positioned, given their ability to benefit from improving liquidity conditions, lower funding costs and expanding access to offshore capital.

Government bonds typically capture the initial repricing as markets adjust to lower macro and external risks. Corporate credit, however, is often where those benefits are ultimately transmitted and monetized through tighter spreads and a lower cost of capital.

That distinction matters for investors. While a rally in sovereign bonds can generate gains through falling yields, high-quality corporate bonds offer the potential to benefit from both declining benchmark rates and spread compression. The combination has the potential to create a powerful total-return opportunity than duration alone.

The first-order trade may be government bonds. The second-order trade may be high-quality corporate credit. And historically, it is often the second-order trade that has delivered a compelling outcome.

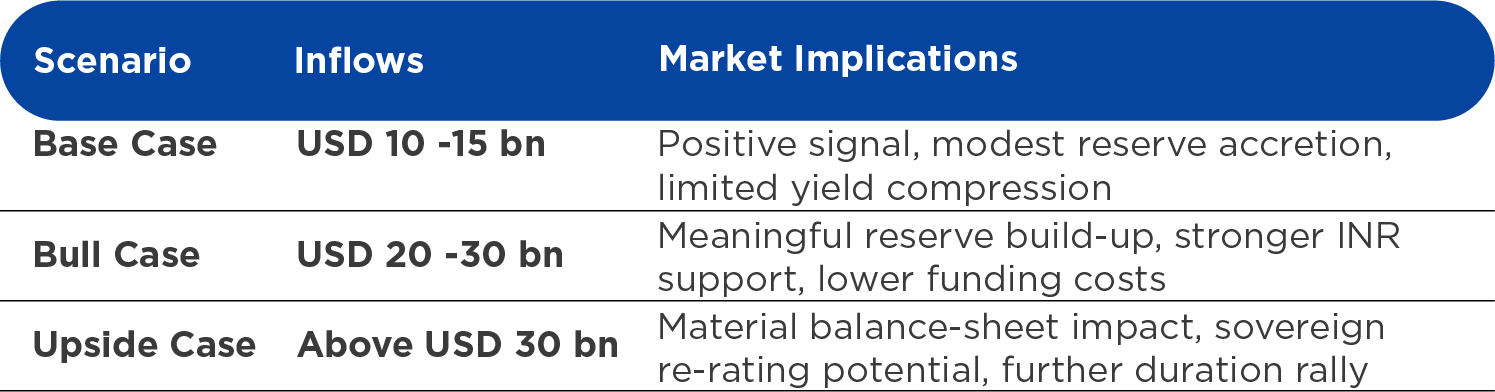

How Large Could the Inflows Potentially Be?

This is perhaps the most debated question surrounding FCNR 2.0.

The market's fixation on whether the programme can replicate the USD 34 billion raised in 2013 may underestimate the opportunity.

The structure today is arguably more supportive than it was thirteen years ago.

For FCNR(B) deposits:

• Banks bear no hedging cost versus approximately 3.5% in 2013.

• Deposits remain exempt from CRR and SLR 1requirements.

• Leverage is expected to be permitted through SBLC structures.

For ECBs:

• Eligibility has expanded to both banks and PSUs.

• The RBI swap facility offers a fixed 1.5% hedging cost.

• Borrowers gain greater certainty around funding costs.

Taken together, these features create stronger economic incentives than those available in 2013.

While the original programme mobilized approximately USD 34 billion (equivalent to 13% of India's foreign exchange reserves at the time), the current reserve base exceeds USD 680 billion.

As a result, inflows of USD 30-50 billion do not appear implausible under a successful execution scenario.

Data Source: Quantum Internal estimates

The exact number of inflows would have a significant bearing on the economy, but not to the extent the broader assumption is…

The RBI's June 2026 measures are inevitably being viewed through the lens of 2013. But the comparison only goes so far.

In 2013, FCNR was a defensive tool deployed to address external vulnerability. In 2026, the same instrument is being deployed from a position of strength - supported by a larger reserve buffer, stronger institutions and deeper capital markets.

The real question is therefore not whether FCNR 2.0 can replicate the USD 34 billion raised in 2013. It is whether it can reinforce India's external position, lower the economy's cost of capital and create room for easier domestic financial conditions.

If it succeeds, the benefits will extend well beyond the rupee - supporting government bonds, corporate credit and broader fixed-income markets.

The instrument may be the same. The objective is not.

In 2013, India was defending its balance sheet. In 2026, it is seeking to optimize it.

That may be the clearest indication yet of how far India's macroeconomic narrative has evolved.

1: CRR: Cash Reserve Ratio. SLR: Statutory liquidity Ratio

What Can Investors Do?

For investors, the opportunity is not necessarily about making a binary call on the rupee or attempting to predict the exact scale of FCNR inflows.

The more relevant question is how to position for a market where liquidity conditions may improve, sovereign risk premia could compress and funding costs may gradually move lower.

In such an environment, dynamic bond funds merit consideration.

Unlike traditional duration-oriented funds, dynamic bond funds have the flexibility to actively adjust portfolio duration, maturity profiles and asset allocation as interest-rate expectations evolve. If FCNR-related inflows, ECB issuance and improving liquidity conditions create room for lower yields, a dynamic approach may be better positioned to capture opportunities across different segments of the curve rather than being locked into a static duration profile.

That flexibility becomes particularly valuable when the outlook remains uncertain. While the medium-term direction may be constructive for fixed income, the path is unlikely to be linear. Global rates, oil prices, geopolitical developments and capital flows can all introduce periods of volatility.

Equally important, investors should avoid layering multiple risks in uncertain environments.

When interest-rate uncertainty remains elevated, taking additional credit risk may not always be adequately compensated. A portfolio built around high-quality corporate bonds particularly AAA-rated PSU and quasi-sovereign issuers alongside sovereign securities can provide a balanced way to participate in the opportunity.

In other words, investors need not take both duration risk and credit risk simultaneously.

A blend of government securities and high-quality credit allows investors to benefit from improving liquidity and potential yield compression while maintaining portfolio resilience if market conditions become more volatile.

In a market where the macro backdrop is improving but uncertainty persists , flexibility, liquidity and credit quality may prove valuable than reaching for yield.

For any queries directly linked to the insights and data shared in the newsletter, please reach out to the author - Sneha Pandey, Fund Manager - Fixed Income at [email protected].

For all other queries, please contact Mohit Bhatnagar - Head - Sales, Quantum AMC at [email protected] / [email protected] or call him on Tel: 9987524548

Read our last few Debt Market Observer write-ups -

- Can the RBI Continue to Defend the Rupee

- India’s Macro Backdrop: Past Fragility, Present Strength

Disclaimer, Statutory Details & Risk Factors:The views expressed here in this article / video are for general information and reading purpose only and do not constitute any guidelines and recommendations on any course of action to be followed by the reader. Quantum AMC / Quantum Mutual Fund is not guaranteeing / offering / communicating any indicative yield on investments made in the scheme(s). The views are not meant to serve as a professional guide / investment advice / intended to be an offer or solicitation for the purchase or sale of any financial product or instrument or mutual fund units for the reader. The article has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. Whilst no action has been solicited based upon the information provided herein, due care has been taken to ensure that the facts are accurate and views given are fair and reasonable as on date. Readers of this article should rely on information/data arising out of their own investigations and advised to seek independent professional advice and arrive at an informed decision before making any investments. Mutual Fund investments are subject to market risks, read all scheme related documents carefully. |

View All

Related Posts

-

What Does the West Asia Crisis Mean for India’s Economy?

Posted On Tuesday, Mar 24, 2026

Over the past few years, geopolitics has steadily returned to the center of global economic discussions.

Read More -

Looking Beyond the 10-Year Benchmark: Decoding India’s Bond Market Signals

Posted On Thursday, Feb 26, 2026

If you glance at India’s financial headlines today, the tone feels reassuring.

Read More -

Positioning for Disinflation

Posted On Friday, Jan 27, 2023

We are well past the peak inflation of 2022. Yet, inflation continues to be the focal point of all the policy discussions and investment thesis in 2023.

Read More