Debt monthly view for October 2022

Posted On Monday, Nov 07, 2022

Bond market was range bound in October 2022. The 10 year maturity government bond was (Gsec) trading between a broad range of 7.35% and 7.55%. On monthly closing basis, the 10 year Gsec settled 5 basis points higher at 7.45% on October 31, 2022 versus 7.40% on September 30, 2022. In 2022 so far, the 10 year yield has moved up 100 basis points.

Money market rates continued to move higher with 3 months treasury bill moving up by 35 basis points during the month from 6.09% on September 30, 2022 to 6.44% on October 31, 2022. In 2022 so far, the 3 month treasury bill yield is up 280 basis points.

Liquidity condition continued to tighten due to increased cash withdrawals and forex sale by the RBI. Liquidity surplus in the banking system as measured by banks’ net lending or borrowing under the RBI’s liquidity adjustment faciality (Repo, SDF, MSF etc.), declined from average of ~Rs. 760 billion during September to average of ~Rs. 35 billion in October 2022. It was around Rs. 7 trillion at start of the year.

Global market’s volatility increased further during October as bond yields across developed markets moved up sharply by the middle of the month and retraced back partially by the month end. The 10 year US treasury yield shoot up from 3.83% to 4.24% and then fell back to close the month at 4.04%. Similarly, the 10 year German bund yield jumped from 2.1% to 2.41% and then fell back to 2.14% by the October end.

In the United Kingdom, the bond market (Gilt) continued to witness extreme volatility since the controversial tax cut proposal by the UK government in September. Long term gilt yields had shot more than 130 basis points in matter of 7 days. It triggered a panic selling by pension funds due to large losses on their leveraged positions and forced the Bank of England to announce bond buying to cool off the market.

Later, in October, the government withdrew the tax cut proposal and instead announce further tightening of fiscal policy. Following all the policy flipflops, the 10 year gilt yield first jumped from 3.2% on September 19, 2022 to 4.5% by mid-October and then fell back down to 3.5% by end of the month.

Turbulence in the gilt market was though started by a bad fiscal policy, the market reaction was compounded due lack of market liquidity and investors’ nervousness given the fast pace of rate hikes around the developed world.

Investors have been complaining of similar lack of liquidity in the US treasury markets. In Japan also trading dried up completely in the 10-year benchmark bond for four consecutive sessions.

With these incidents, financial stability concerns have resurfaced. There is a worry that fast pace of rate hikes in the developed world would further deteriorate the liquidity in the financial market.

In India, the RBI followed the expected path and delivered another rate hike of 50 basis points on September 30, 2022. This took the Repo rate to 5.9% and the SDF rate to 5.65%. Since April this year, the RBI has frontloaded the monetary policy tightening with - (a) 190 basis points increase in the repo rate; (b) 230 basis points increase in the floor policy rate (Reverse Repo/SDF); and (c) reduction in core liquidity surplus by around Rs. 7 trillion.

Impact of these rate hikes and liquidity tightening will be seen in the real economy over the next 3-4 quarters. Given the significant frontloaded tightening in monetary policy and fragility of economic growth, there is a case for the RBI to slowdown or even pause.

Some of the MPC (monetary policy committee) members also presented a case for the RBI to adopt a more calibrated approach going forward and warned of harmful effects of overtightening in an environment where the growth outlook is very fragile. In our opinion, the RBI will be more data dependent and will likely slow down the pace of tightening. The Repo rate may peak somewhere between 6.0%-6.5%.

The bond market is already pricing for a terminal repo rate of 6.5%. So, another 25-50 basis points repo rate hike will not impact market prices in any material way.

We believe, the peak of central banks’ hawkishness is now behind us. It is a time we should look beyond the market noises and spot the emerging opportunities in the bond market.

After recent sell off, bond valuations have improved. Currently, the 3-5 years government bonds are trading at yield of between 7.30%-7.45%. This is more than 140 basis points above the repo rate of 5.9%. The long-term average of this spread in a tightening interest rate environment is around 80-90 basis points.

As the monetary policy stabilises, yield spread between long term bonds and the repo rate should compress. So, we see limited upside on yields from here. Even in terms of real interest rates, entire bond yield curve is now trading at a yield above the expected CPI inflation.

We expect bond yields to move sideways in a tight range with the 10 year Gsec yield trading between 7.2%-7.6%. While Short term money market rates will move higher along with the policy repo rate.

Considering the duration-accrual balance, 3-5 year segment remains the best play as core portfolio allocation. However, valuation at the longer end bonds upto 10 year have also turned attractive after recent sell off.

We suggest investors with 2-3 years holding period should consider adding their allocation to dynamic bond funds to benefit from higher yields on medium to long term bonds.

Dynamic bond funds have flexibility to change the portfolio positioning as per the evolving market conditions. This makes dynamic bond funds better suited for the long-term investors in this volatile macro environment.

Investors with shorter investment horizon and low risk appetite should stick with liquid funds. With increase in short term interest rates, we should expect further improvement in potential returns from investments in liquid funds going forward.

Since the interest rate on bank saving accounts are not likely to increase quickly while the returns from liquid fund are already seeing an increase, investing in liquid funds looks more attractive for your surplus funds.

Investors with a short-term investment horizon and with little desire to take risks, should invest in liquid funds which own government securities and do not invest in private sector companies which carry lower liquidity and higher risk of capital loss in case of default.

Source: RBI

| Name of the Scheme | This product is suitable for investors who are seeking* | Riskometer |

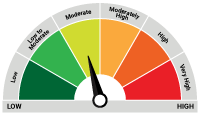

| Quantum Dynamic Bond Fund An Open-ended Dynamic Debt Scheme Investing Across Duration. A relatively high interest rate risk and relatively low credit risk. | • Regular income over short to medium term and capital appreciation • Investment in Debt / Money Market Instruments / Government Securities |  Investors understand that their principal will be at Low to Moderate Risk |

*Investors should consult their financial advisers if in doubt about whether the product is suitable for them.

The Risk Level of the Scheme in the Risk O Meter is based on the portfolio of the scheme as on October 31, 2022.

| Potential Risk Class Matrix – Quantum Dynamic Bond Fund | |||

| Credit Risk → | Relatively Low | Moderate (Class B) | Relatively High (Class C) |

| Interest Rate Risk↓ | |||

| Relatively Low (Class I) | |||

| Moderate (Class II) | |||

| Relatively High (Class III) | A-III | ||

Disclaimer, Statutory Details & Risk Factors:The views expressed here in this article / video are for general information and reading purpose only and do not constitute any guidelines and recommendations on any course of action to be followed by the reader. Quantum AMC / Quantum Mutual Fund is not guaranteeing / offering / communicating any indicative yield on investments made in the scheme(s). The views are not meant to serve as a professional guide / investment advice / intended to be an offer or solicitation for the purchase or sale of any financial product or instrument or mutual fund units for the reader. The article has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. Whilst no action has been solicited based upon the information provided herein, due care has been taken to ensure that the facts are accurate and views given are fair and reasonable as on date. Readers of this article should rely on information/data arising out of their own investigations and advised to seek independent professional advice and arrive at an informed decision before making any investments. Mutual fund investments are subject to market risks read all scheme related documents carefully.Please visit – www.QuantumAMC.com to read scheme specific risk factors. Investors in the Scheme(s) are not being offered a guaranteed or assured rate of return and there can be no assurance that the schemes objective will be achieved and the NAV of the scheme(s) may go up and down depending upon the factors and forces affecting securities market. Investment in mutual fund units involves investment risk such as trading volumes, settlement risk, liquidity risk, default risk including possible loss of capital. Past performance of the sponsor / AMC / Mutual Fund does not indicate the future performance of the Scheme(s). Statutory Details: Quantum Mutual Fund (the Fund) has been constituted as a Trust under the Indian Trusts Act, 1882. Sponsor: Quantum Advisors Private Limited. (liability of Sponsor limited to Rs. 1,00,000/-) Trustee: Quantum Trustee Company Private Limited. Investment Manager: Quantum Asset Management Company Private Limited. The Sponsor, Trustee and Investment Manager are incorporated under the Companies Act, 1956. |

Related Posts

-

Debt Monthly for March 2026

Posted On Monday, Mar 02, 2026

As FY26 draws to a close, India’s bond markets sit at the crossroads of macro stability

Read More -

Debt Monthly for February 2026

Posted On Monday, Feb 02, 2026

In FYTD26, Indian bond yields defied expectations, firming up even as monetary policy turned supportive.

Read More -

Debt Monthly for January 2026

Posted On Thursday, Jan 01, 2026

Navigating 2026: India’s Bond Market in a Changing Global Landscape

Read More