Debt Monthly for November 2025

Posted On Tuesday, Nov 04, 2025

October 2025 in a Nutshell: Monetary Policy and Demand–Supply

If we had to sum up October in two words - it would be Monetary Policy and Demand–Supply.

The month began with the Reserve Bank of India (RBI) keeping both interest rates and its policy stance unchanged. However, the tone of the announcement was more dovish — meaning the RBI sounded more open to supporting growth rather than worrying too much about inflation.

Interestingly, two external members of the Monetary Policy Committee (MPC) even voted for changing the stance back to “accommodative,” which would signal a stronger bias toward rate cuts in the future.

The RBI’s meeting minutes clearly highlight that growth remains the central focus. While policymakers were confident about robust performance in Q1 and Q2 FY26, they also discussed emerging concerns for the latter half of the year. The primary headwinds stem from weaker export trends and softening investment momentum, largely influenced by recent U.S. tariff measures that have dampened global trade sentiment.

On the inflation front, policymakers seemed more relaxed. Cooling food prices and recent GST rate reductions have helped bring down inflation expectations. The near-term inflation outlook looks comfortable, though a few members did caution that prices might edge up again in FY27 as demand strengthens. For now, the RBI appears to be in “wait and watch” mode, choosing to hold its ground until it gains clarity from upcoming trade negotiations, festive season demand trends, and the Q2 GDP print.

Markets were pricing in a small chance of a rate cut (about 25 basis points) in December 2025. But that expectation has now faded slightly after global agencies (including the IMF) raised India’s growth forecasts to beyond the RBI’s target of 6.5% for FY 26.

Simply put, stronger growth reduces the case for further immediate rate cuts by the RBI, despite having enough policy room for rate cuts.

Market Dynamics: A Tug of War Between Demand and Supply

Bond markets have been witnessing their own push-and-pull. While the supply of government bonds has remained manageable, demand for longer-dated bonds has become unpredictable. This comes despite the appealing yield spreads between 10-year bonds and longer-dated maturities in the 30–40-year segment.

Globally, both the European Central Bank (ECB) and the Bank of Japan kept their policy rates unchanged, while the U.S. Federal Reserve implemented a 25 basis points rate cut during the month. This move should have ideally supported both U.S. and Indian debt markets. However, Fed Chair Jerome Powell’s hawkish tone (signaling caution about more cuts) left investors uncertain.

As a result, the 10-year U.S. Treasury yield fluctuated between 3.9% and 4.15% through October, while India’s 10-year government bond yield stayed within a narrow 6.49%–6.59% range.

Money market yields ended the month broadly flat, though they witnessed some rangebound movement amid fluctuations in system liquidity. Liquidity conditions briefly slipped into deficit by around ₹70,000 crore during the month - prompting the RBI to step in through Variable Rate Repo (VRR) operations. By month-end, however, system liquidity returned to a surplus of about ₹1.2 trillion, supported by government spending, while core liquidity stood at roughly ₹4 trillion for the week ended October 17, 2025.

T-bill yields in the 3-month segment remained largely unchanged at 5.4%, whereas 3-month AAA-rated PSU CP/CD rates inched up slightly to 6% levels at the end of the month.

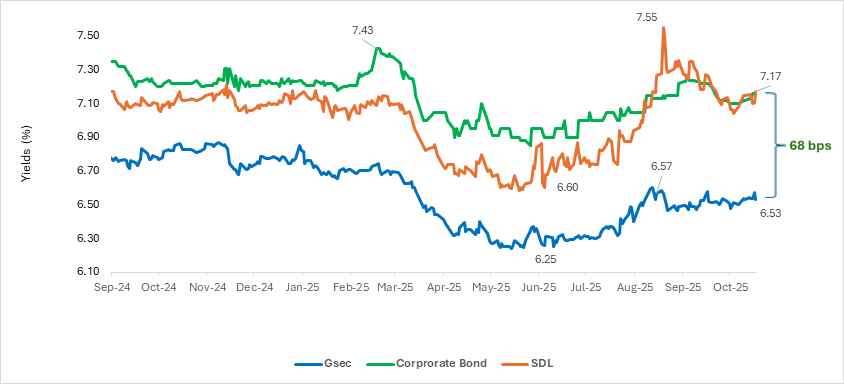

The corporate bond yield curve also steepened during the month, with the spread between 10-year corporate bonds and 10-year G-Secs narrowing to around 68 basis points by month-end. Despite this compression, investor demand for corporate bonds has remained strong. On the other hand, primary supply appears to have moderated, leading to a notable narrowing in spreads between State Development Loans (SDLs) and corporate bonds.

Chart I: Spreads between SDLs and Corporate bonds have narrowed significantly

This chart shows the yield spreads between Government Securities (G-Secs), State Development Loans (SDLs), and corporate bonds over time. It highlights that the difference in yields (spreads) between SDLs and corporate bonds has narrowed significantly. Corporate bond yields generally track above G-Secs, while SDLs show higher volatility with occasional spikes. The current spread is around 68 basis points, indicating tighter risk premiums. Overall, the trend suggests improved credit conditions and stronger investor confidence in corporate debt markets.

Source: Bloomberg. Above data is for the yields on the 10- year maturity of respective bond for the last twelve months - September 2024 to October 2025. Data on corporate bond yields is for AAA PSU corporate bonds.

What to Watch Next

The next few data points - especially October’s CPI (inflation) print and the impact of the new GST 2.0 rates on festive season demand (growth front) - will be crucial. If domestic growth remains strong and trade negotiations turn favorable, the RBI may prefer to hold off on additional rate cuts.

That said, our base case still assumes one final 25 basis point cut, likely taking the repo rate to 5.25% in FY26, before the central bank enters a prolonged pause phase. This would mark the end of the current easing cycle.

On the fiscal side, the central government appears on track to meet its target deficit. Lower subsidy spending and healthy proceeds from disinvestments may help offset any shortfall in tax collections. The key question for next year will be how the government balances growth spending with fiscal discipline.

In this phase, we expect the yield curve to steepen (benefiting the shorter end of the yield curve) and markets are likely to remain largely rangebound and data dependent. In other words - we don’t expect a big bond rally, but also no major rate hikes anytime soon either.

What can investors do?

For investors, this backdrop continues to favor spread assets such as State Development Loans (SDLs) and high-quality (AAA Rated) corporate bonds with a slightly lower duration. These instruments offer better yields without taking on excessive risk.

However, it’s important to stay cautious about credit and liquidity risks. Portfolios that mix AAA-rated corporate bonds with government securities (G-Secs) can provide a good balance between safety and return.

For investors with shorter investment horizons and a low risk tolerance, liquid funds remain the more suitable option.

Source: Reserve Bank of India (RBI), Ministry of Statistics & Program Implementation (MOSPI), Bloomberg

Disclaimer, Statutory Details & Risk Factors:

The views expressed here in this article / video are for general information and reading purpose only and do not constitute any guidelines and recommendations on any course of action to be followed by the reader. Quantum AMC / Quantum Mutual Fund is not guaranteeing / offering / communicating any indicative yield on investments made in the scheme(s). The views are not meant to serve as a professional guide / investment advice / intended to be an offer or solicitation for the purchase or sale of any financial product or instrument or mutual fund units for the reader. The article has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. Whilst no action has been solicited based upon the information provided herein, due care has been taken to ensure that the facts are accurate and views given are fair and reasonable as on date. Readers of this article should rely on information/data arising out of their own investigations and advised to seek independent professional advice and arrive at an informed decision before making any investments.

Mutual fund investments are subject to market risks read all scheme related documents carefully.

View All

Related Posts

-

Debt Monthly for May 2026

Posted On Monday, May 04, 2026

India’s debt markets heading into May 2026 appear set to remain range-bound, albeit with underlying fragility.

Read More -

Debt Monthly for April 2026

Posted On Wednesday, Apr 01, 2026

The month of April opens with India’s bond markets caught in the crosscurrents of global turmoil.

Read More -

Debt Monthly for March 2026

Posted On Monday, Mar 02, 2026

As FY26 draws to a close, India’s bond markets sit at the crossroads of macro stability

Read More