Equity monthly view for December 2021

Posted On Friday, Jan 01, 2021

January 01, 2021

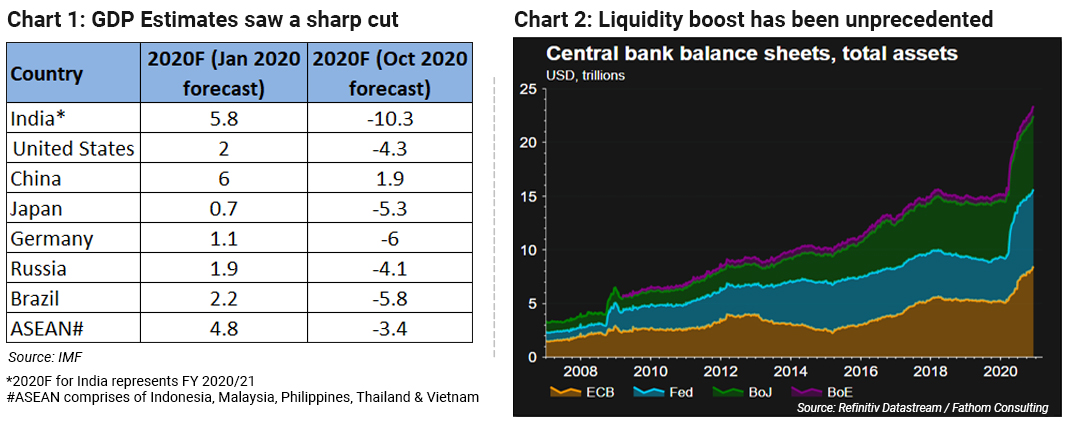

This has been a year like no other, who would have thought after the ~39% collapse from the high achieved in January 2020, the S&P Sensex would actually end the year at all-time highs, giving a YTD return of ~16%. This has also been a year which reinforced the notion that traditional valuation metrics may not work in a world where central banks continue to pump massive liquidity and cost of capital continues to be pushed lower. Equity markets have ignored sharp cuts in GDP growth and significant loss of jobs & income and continued to rally, driving valuations much above historically observed levels.

The Covid virus which continues to rage, initially looked like a China specific problem and companies importing from China scrambled to make alternate arrangements. However it quickly spread to the rest of the world and country after country realized, the only way to not overwhelm the healthcare infrastructure was to halt human contact, to slow down the virus spread. Lockdowns were announced by almost all the big economies leading to a collapse in economic activity. Governments responded by opening the fiscal tap and nudged central bankers to ease liquidity to reduce the economic damage caused by strict lockdowns.

India which was reeling under an economic slowdown even before Covid struck was late to react. The lockdown announced from March 23, 2020 onwards was one of the strictest in the world. Unlike the developed world which launched a strong fiscal response to counter the impact of a lockdown, the Indian Government had limited fiscal space and launched a feeble fiscal package and leaned on the RBI to boost liquidity and rollover debt payments to ensure financial markets did not freeze and viable businesses get some breathing space. The lack of a strong fiscal response resulted in GDP contracting by ~24% in Q1FY21, one of the sharpest contraction in GDP growth amongst major economies.

The rebound post the contraction in the GDP has been robust, Rural India which was largely unaffected from the lockdown and sitting on a record harvest drove the initial leg of the demand recovery. Pent up demand from urban centers post the unlock, quickly followed and companies were operating at 90%-100% of their normalized operations by September. Barring a few specific industries like Hospitality and Aviation most industries had come back to some normalcy by Q3FY21.

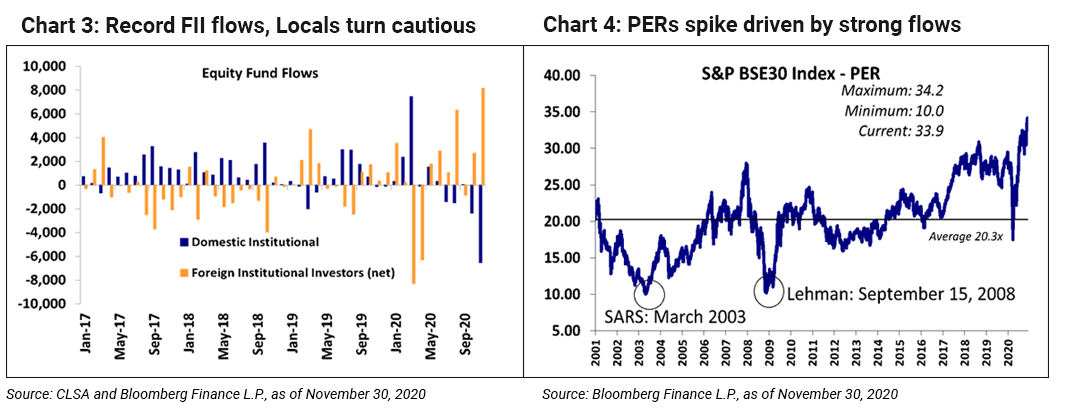

India has always drawn its share of FII flows and this year has been a record. India, which experienced one of the largest single month outflow in March 2020 (~ USD 8bn), will end the year will net inflows of USD 22 bn with ~USD 16 bn coming in just the last two months of the calendar year. Local mutual funds have seen redemptions with net selling of ~USD 6.5 bn, as retail investors have used the rally to book profits. Record FII flows have raised PERs and the market now trades at multiples which warrant caution (though overstated due to contraction in earnings in Q1FY21).

Market Outlook

Despite the elevated valuations and sub-par economic growth, we are more optimistic today about Investing in equities than we were a year earlier for the following reasons:

• Interest rates for mortgages are at a two decade low. Coupled with lower real estate prices and reduced transaction charges, affordability has improved by ~15-20%. This could drive increased buying activity. Increased real estate transactions could drive consumer demand as buyers look to fill up newly purchased homes with consumer durables, home furnishings etc. boosting economic activity

• Indian G-sec yields at ~6% appear far more attractive than yields currently on offer in the western world (zero to negative). If Oil prices remain low, the rupee may not see sharp depreciation, making Indian fixed income yields attractive to Pensions in the west searching for yield. India could potentially draw significant flows from this pool, which if channeled correctly can keep domestic interest rates low and act as an economic multiplier to drive consumption demand as well as Infrastructure creation.

• Corporate India having experienced an economic slowdown for the last few years has been focused on driving efficiency and controlling costs. Even a small rebound in demand will drive operating leverage, resulting in profits rising at a much faster pace than revenues

• Strong Flows plus an improving earning cycle, will most likely ensure elevated PERs sustain

Resurgence of Covid cases, rising inflation and disruptive Government Policy making are key risks to our thesis and could stall an economic recovery. Elevated valuations also means returns expectation need to be moderated and downside risks are now higher.

Value stocks which have been out of favour in the last few years due to slow economic growth have done well over the last few months as economic growth rebounds and they narrow the growth differential, reducing valuation discount visa vie growths stocks. If an economic recovery were to sustain, one can expect value stocks to continue to do well.

The Equity Portfolio team used the collapse in February and March 2020 to add new names to the portfolio at attractive valuations and our cash levels which was ~ 9% in January 2020, came down to less than 5% by March 2020. The focus was to ensure we add companies who are high quality in terms of balance sheet strength and management capability and will be able to survive the impact of a prolonged lockdown. We had also stress tested our entire portfolio to ensure all our investee companies have adequate cash on books/ low leverage, to survive the lockdown. Post the rally we have booked profits in select names due to expensive valuations and resized weights in certain stocks based on our risk perception. We believe we have built a good portfolio of companies which will do well over the next few years as economic conditions normalize.

Indian equities remain an attractive asset class and is expected to do well over the long term. Investors are advised to remain invested. Trying to time market entry and exit may backfire. SIPs remain the simplest way to tide over market cycles. 2020 has also been a wakeup call for a balanced asset allocation plan and Investors are advised to ensure they spread their savings across Equity, Debt and Gold based on their long term goals and risk & return preferences.

Source: Bloomberg

Disclaimer, Statutory Details & Risk Factors:

The views expressed here in this article / video are for general information and reading purpose only and do not constitute any guidelines and recommendations on any course of action to be followed by the reader. Quantum AMC / Quantum Mutual Fund is not guaranteeing / offering / communicating any indicative yield on investments made in the scheme(s). The views are not meant to serve as a professional guide / investment advice / intended to be an offer or solicitation for the purchase or sale of any financial product or instrument or mutual fund units for the reader. The article has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. Whilst no action has been solicited based upon the information provided herein, due care has been taken to ensure that the facts are accurate and views given are fair and reasonable as on date. Readers of this article should rely on information/data arising out of their own investigations and advised to seek independent professional advice and arrive at an informed decision before making any investments.

Mutual fund investments are subject to market risks read all scheme related documents carefully.

Please visit – www.QuantumMF.com to read scheme specific risk factors. Investors in the Scheme(s) are not being offered a guaranteed or assured rate of return and there can be no assurance that the schemes objective will be achieved and the NAV of the scheme(s) may go up and down depending upon the factors and forces affecting securities market. Investment in mutual fund units involves investment risk such as trading volumes, settlement risk, liquidity risk, default risk including possible loss of capital. Past performance of the sponsor / AMC / Mutual Fund does not indicate the future performance of the Scheme(s). Statutory Details: Quantum Mutual Fund (the Fund) has been constituted as a Trust under the Indian Trusts Act, 1882. Sponsor: Quantum Advisors Private Limited. (liability of Sponsor limited to Rs. 1,00,000/-) Trustee: Quantum Trustee Company Private Limited. Investment Manager: Quantum Asset Management Company Private Limited. The Sponsor, Trustee and Investment Manager are incorporated under the Companies Act, 1956.

View All

Related Posts

-

Equity Outlook - August 2026

Posted On Monday, Aug 03, 2026

Indian equities were flat in the month of July, as the West Asia crisis re-escalated. Flair up in the West Asia conflict resulted in crude

Read More -

Equity Outlook - July 2026

Posted On Wednesday, Jul 01, 2026

Indian equities recovered in the month of June, as the West Asia crisis showed signs of de-escalation.

Read More -

Equity Outlook - June 2026

Posted On Monday, Jun 01, 2026

Markets were marginally higher in the month of May. Following table shows the change in broad market cap indices.

Read More