|

|

|

Clarification: There was a typo error in the email sent to you yesterday, the same has been rectified in this email. We sincerely apologize for the inconvenience caused.

Many so called financial analysts and pundits claim that the job of an equity fund is to be invested fully in equities. Nothing wrong with the sentiment since it is, in some sense, true that an equity fund should be invested in equities! The investor has put his/her hard earned money into the fund and expects good returns and not returns in line with savings bank accounts.

However a quote on investing goes, "The stock market is a no-called-strike game. You don't have to swing at everything - you can wait for your pitch." Which means a true value investor waits for the correct opportunity to buy or sell stocks and is not swayed into action by market levels. Thus implying he may end up with cash while waiting for the opportune time to invest.

Therefore is it correct to conclude that any equity fund which is almost fully invested in the market and has low cash levels is good and any equity fund with high cash levels is a bad fund???

Ummm...Not necessarily... and this article is all about busting this myth. Read on to know why.

True value investing and QLTEF

Quantum follows the value investment style while investing. Among the most important tenets of value investing# is the concept of having a decent margin of safety. In simple terms this means that securities should be bought at significant discount to their intrinsic value (or true worth) - for example, paying only Rs.65 for a stock one believes is worth Rs. 100. Another important element of value investing is the emphasis on safety of capital. Value investors focus heavily on not losing money by avoiding investment calls that can result in significant losses. Still another principle of value investing is that it should be expected to give adequate return. Now "adequate", according to the father of value investing meant, "any rate or amount of return, however low, which the investor is willing to accept, provided he acts with reasonable intelligence." For an actively managed mutual fund the lowest acceptable return could be that of its benchmark, plus costs of managing the Scheme, over a sufficiently long time.

True to the value investing principles, we buy when we believe a company's valuation is cheap relative to its long term earning potential and historical valuations and we sell when we believe a company's valuation is expensive based on the long term earnings potential and historical valuations. This analysis is at a stock level and not at the Index level. Whenever our pre-determined buy limit for a stock is triggered, the company becomes part of the portfolio and whenever a sell limit is triggered we exit the stock. Whatever remains is cash.

Therefore when the markets are running up on sentiment - we will not invest in stocks with inflated values, hence the cash level will be high. Now the markets are back at a level that they were before the election of the 'new' government. We believe it was sentiment that drove the S&P BSE Sensex up to almost 30,000 levels, now that the initial sheen seems to have worn off the markets are below the 24,000 mark, at the time of writing this article.

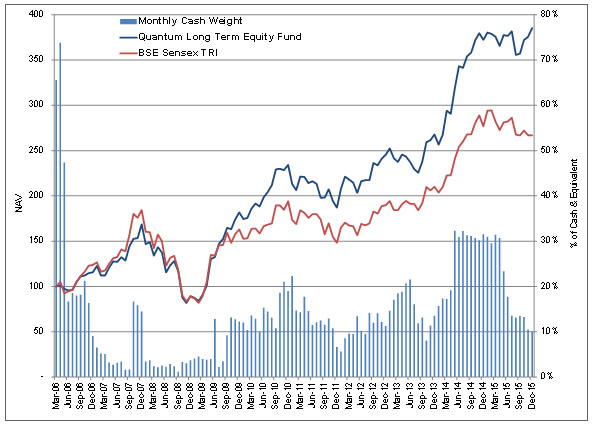

Here is a chart that defines the relationship of cash levels of QLTEF, with its actual performance vis-a-vis the benchmark (S&P BSE 30 TRI). The detailed performance is covered in one of the following paragraphs, "What about the numbers? How have the peers performed, and the benchmark?"

|

|

| Source: Bloomberg. Past performance may or may not be sustained in the future

|

What this graph shows is that as we look at the record of the Quantum Long Term Equity Fund the average cash level of the fund, since its inception in March 2006, is 14.5%.

One of the 'residual' effects of having high cash levels is that by staying in cash we reduce risk that an investor is exposed to, in an extremely volatile market. There are times when we need to be aggressive and buy stocks, and there are times when we need to be a little circumspect and hold on, rather than taking the plunge. One of the gems of value investing is "Be fearful when others are greedy and to be greedy only when others are fearful."

The best way of remaining fearful when others are greedy is to not invest in choppy markets, but wait for calm seas to start sailing in the investment world.

That timing question again - Are we trying to time the markets?

We do not look at Index levels to decide equity allocation. We do not believe we have that capability. What we do believe is we have the capability to look at an individual company and determine whether it is trading at a discount to its intrinsic value. Market levels are not a consideration when deciding whether a company should be part of the portfolio. If we do find companies offering value even at these elevated market levels (and we continue to actively research companies factoring latest inputs in our research models), they will become a part of the portfolio.

Here is the gist of our investment process:

We follow a bottom-up stock selection process depicted as below -

| Clients get best of bottom up ideas with a risk control measurement for each sector < 40 stocks |

|

Portfolio of stocks with broad exposure to various sectors

Reflecting three broad themes: domestic consumption, exports and infrastructure |

|

| Regular meeting to review ideas and approve value stocks for the database

100 stocks |

|

| Analysts study stocks in their sector in India with global comparisons wherever necessary. The universe is generally S&P BSE 200 with flexibility to include new issues. Research includes visit notes, financial models and investment thesis, supplemented with broker research >200 stocks |

And the following guidelines are part of the portfolio construction

| 1. |

Stock has to be under active and current coverage; average daily trading volume of US$ 1 million |

| 2. |

Every stock in the AMC's database has a pre-assigned Buy / Sell Limit. This is an INR price based on underlying fundamental sector criteria. |

| 3. |

The AMC generally buys a new stock at the pre-determined Buy price (or below) and generally sells an existing stock at the pre-determined Sell price or above. It may add to a stock the Scheme already owns if it is between the pre-determined Buy and Sell price. |

| 4. |

For the sake of a benchmark the AMC uses the S&P BSE 30 TRI. The AMC is indifferent to whether a stock, the Scheme owns, is in the S&P BSE 30 TRI or not - although it recognizes its effect on liquidity. |

| 5. |

The AMC does not make sector calls. It makes stock calls. |

What about the numbers? How have the peers performed, and the benchmark?

The proof of the pudding - for any fund - is in the numbers! While we cannot compare the performance of the Quantum Long Term Equity Fund with that of its peers, if we look at the returns since inception vis-a-vis the benchmark, here is where we stand.

|

| |

| Period |

Scheme^ |

BSE- 30 TRI Returns |

BSE Sensex Returns |

CRISIL - AMFI Large Cap Fund Performance Index$ |

Value of investment of Rs. 10,000@ |

| Scheme (RS.) |

BSE- 30 TRI (RS.) |

BSE Sensex (RS.) |

CRISIL - AMFI Large Cap Fund Performance Index |

| Dec 31, 2014 to Dec 31, 2015 |

3.49% |

-3.68% |

-5.03% |

-1.51% |

10,349 |

9,632 |

9,497 |

9,849 |

| Dec 31, 2013 to Dec 31, 2014 |

38.98% |

31.87% |

29.89% |

39.38% |

13,898 |

13,187 |

12,989 |

13,938 |

| Dec 31, 2012 to Dec 31, 2013 |

9.16% |

10.70% |

8.98% |

5.74% |

10,916 |

11,070 |

10,898 |

10,574 |

| Since Inception ** |

15.01% |

11.01% |

9.42% |

11.45% |

39,410 |

27,862 |

24,175 |

28,966 |

^ Past performance may or may not be sustained in the future. Performance of the Dividend option for the investor would be net of the dividend distribution tax, as applicable. **Date of Inception - March 13, 2006.

$ For methodology please refer the bottom of this mailer

To view performance of all schemes managed by Fund Manager Mr. Atul Kumar please refer to the Factsheet. |

|

| |

|

Looking at risk adjusted returns against the benchmark...

|

| Risk measure |

QLTEF |

BSE- 30 TRI |

BSE Sensex |

| Sharpe ratio |

0.46 |

0.23 |

0.12 |

| Note: Risk free return as on 8 February, 2016. Source: Valueresearch |

|

Sharpe ratio is the average return earned per unit of risk undertaken by the fund. Therefore higher the Sharpe ratio of the fund, the better it is, since the ratio denotes the amount of return that the investor get for every unit of risk undertaken by the fund manager. Since it is a ratio, the closer it is to 1 the better. As per the table above QLTEF has a better Sharpe ratio than the S&P BSE Sensex and its benchmark - the S&P BSE 30 TRI.

In addition, one can always log onto websites which compare fund performance to see where QLTEF stands amongst its peers. Thanks to the process-driven stock picking process that has been in place since inception.

QLTEF is a low turnover fund

Apart from the fact that our investing philosophy and process result in QLTEF being high in cash sometimes, an equally distinguishing fact is that we are traditionally a low portfolio turnover fund. Portfolio turnover ratio is a measure that tells how frequently a fund manager changes his portfolio by buying or selling securities in the portfolio. Frequent churning of a portfolio is undesirable for two reasons. Firstly it increases the transaction costs. Secondly it could signify the lack of a strong long term view on securities in the portfolio.

Our long term approach means that we follow a buy and hold strategy for the securities that enter our portfolio. This results in a low portfolio turnover ratio. That said portfolio turnover should always be considered for a sufficiently long duration. The table below shows the portfolio turnover of QLTEF over the last 4 years.

| One year period ended | Portfolio Turnover Ratio (PTR) |

| 31 December, 2015 |

6.74% |

| 30 December, 2014 |

22.80% |

| 30 December, 2013 |

24.37% |

| 31 December, 2012 |

14.59% |

Source: Factsheets. Past performance may or may not be sustained in the future.

Typically the portfolio turnover of a value style fund following the buy-and-hold strategy is about 20-30%. PTR of QLTEF is very much in line with what is expected.

To conclude

We believe the secret to building steady, long term sustainable returns in equities lies in buying stocks when they are cheap and selling them when they turn expensive. Buying stocks when they are expensive and hoping to sell them when they turn even more expensive is not a strategy we believe in or are very good at. We continue to stay focused on building a portfolio which delivers long term steady return to the investor.

Therefore we'd like to reiterate that we wish to continue with our tried and tested, disciplined research and investment process; and stay true to our commitment to our investors: deliver sensible, risk-adjusted, long-term returns for clients with a long term investment horizon. And not shy away from cash holdings when it is a result of diligently following our investment philosophy.

Source: #Value investing principles

|

|

|

|

|

|

Risk Factors: Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

Please visit - www.QuantumMF.com to read Scheme Specific Risk Factors. Investors in the Scheme(s) are not being offered a guaranteed or assured rate of return and there can be no assurance that the scheme's objective will be achieved and the NAV of the scheme(s) may go up or down depending upon the factors and forces affecting securities market. Investment in mutual fund units involves investment risks such as trading volumes, settlement risk, liquidity risk, default risk including possible loss of capital. Past performance of the Sponsor / AMC / Mutual Fund does not indicate the future performance of the Scheme(s). Statutory Details: Quantum Mutual Fund (the Fund) has been constituted as a Trust under the Indian Trusts Act, 1882. Sponsor: Quantum Advisors Private Limited. (liability of Sponsor limited to Rs. 1,00,000/-) Trustee: Quantum Trustee Company Private Limited. Investment Manager: Quantum Asset Management Company Private Limited (AMC). The Sponsor, Trustee and Investment Manager are incorporated under the Companies Act, 1956.

CRISIL AMFI MF Performance Indices Methodology:

CRISIL - AMFI MF Performance Indices seeks to track the performance of the mutual funds across various categories. CRISIL - AMFI Large Cap Fund Performance Index is based on large cap funds which are ranked under CRISIL Mutual Fund ranking are part of the index. CRISIL - AMFI ELSS Fund Performance Index is based on ELSS funds which are ranked under CRISIL Mutual Fund ranking are part of the index. CRISIL - AMFI Liquid Fund Performance is based on the liquid funds which are ranked under CRISIL Mutual Fund ranking are part of the index. Total Return Index, is adjusted for corporate action in the mutual fund schemes. Index portfolio is marked-to-market on a daily basis using adjusted Net Asset Value (NAV). Funds which are ranked under CRISIL Mutual Fund ranking are part of the index. Eligibility of funds are based on minimum NAV history and a minimum AUM. Index values are calculated on daily basis using chain-link method. Asset weighted returns and quarterly rebalancing is carried out. CRISIL Limited (CRISIL) has taken due care and caution in preparing this performance based on the information obtained by CRISIL from sources which it considers reliable. CRISIL does not guarantee the accuracy, adequacy or completeness of the Data / information and is not responsible for any errors or omissions or for the results obtained from the use of Data / information. Please refer the website for methodology and disclaimer.

|

|

Quantum Asset Management Company Private Limited

Regd office - 505, Regent Chambers, 5th Floor, Nariman Point, Mumbai - 400021, India

Toll Free No.:1800-209-3863 / 1800-22-3863, Telephone No.:91-22-61447800, Toll Free Fax no.:1800-22-3864

Email: [email protected], Website: www.QuantumMF.com CIN: U65990MH2005PTC156152 | |

|

|